The Goods and Services Tax Network (GSTN) has announced significant enhancements to the e-Way Bill (EWB) system aimed at strengthening the digital compliance framework under GST. While the implementation was originally scheduled for June 2026, it has now been deferred to 1st, August 2026, providing taxpayers, transporters, ERP vendors and software developers additional time to prepare for the changes.

The advisory introduces two major functional enhancements:

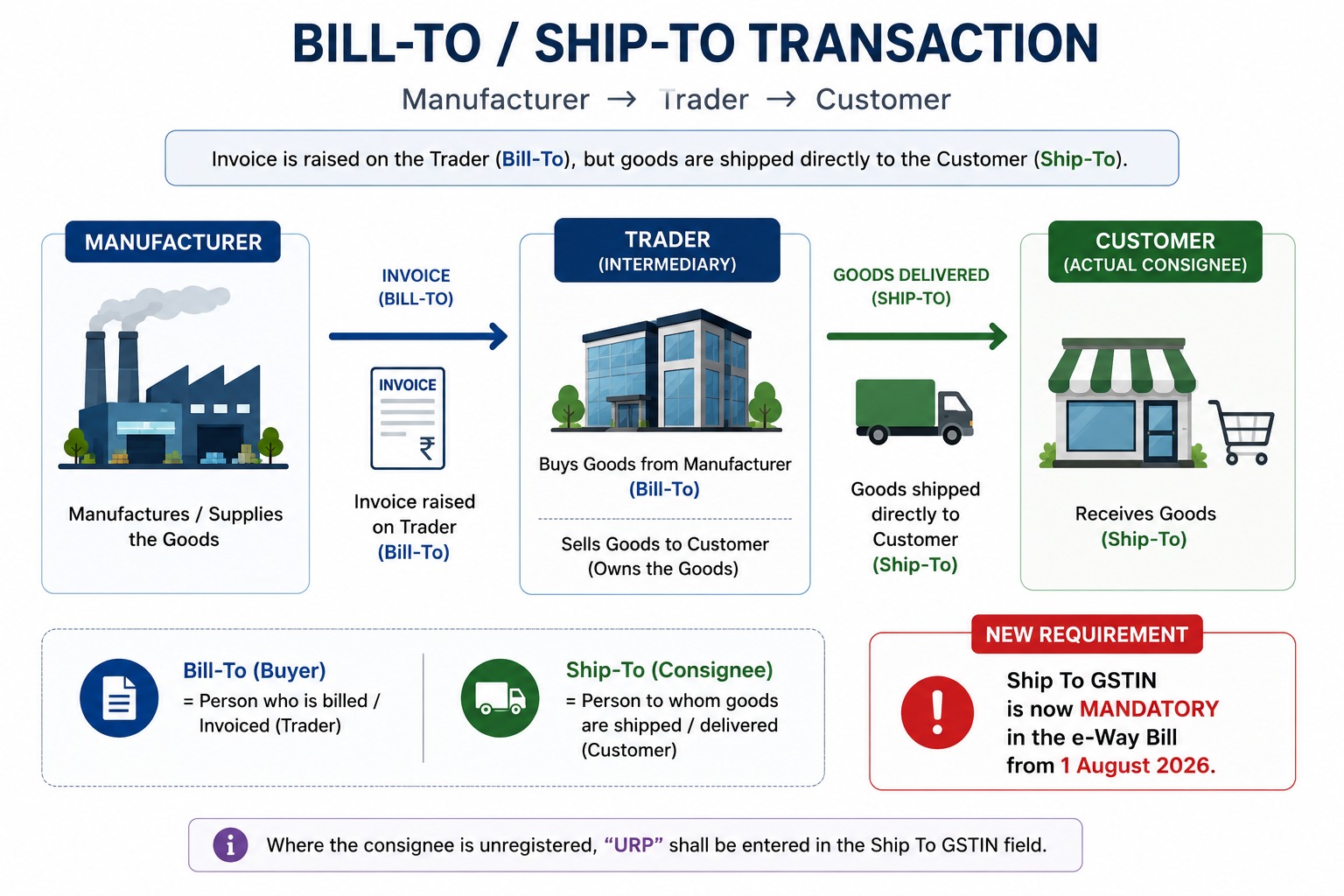

• Mandatory capture of ‘Ship To GSTIN’ in Bill-To / Ship-To transactions.

• Introduction of a Voluntary e-Way Bill Closure facility.

Although these measures are intended to improve traceability and data integrity within the GST ecosystem, they have also generated discussion within the trading community regarding their operational and commercial implications.

We examine both the compliance objectives of the GSTN and the concerns expressed by industry.

1. Mandatory ‘Ship To GSTIN’ in Bill-To / Ship-To Transactions

GSTN has made it mandatory to capture the Ship To GSTIN while generating an e-Way Bill in Bill-To / Ship-To transactions. Where the consignee is an unregistered person, ‘URP’ must be entered.

What is a Bill-To / Ship-To Transaction?

Manufacturer → Trader → Customer

The manufacturer raises the invoice on the trader (Bill-To), while the goods are dispatched directly to the trader’s customer (Ship-To). This model is commonly used in distribution networks, wholesale trade, drop-ship arrangements, third-party logistics and multi-location supply chains.

GSTN’s Objective

• Improve traceability of goods movement.

• Strengthen data integrity.

• Capture the actual destination of goods.

• Improve audit trails.

• Enable better system-driven compliance and analytics.

• Reduce the possibility of misuse of e-Way Bills.

2. Introduction of Voluntary e-Way Bill Closure

GSTN has introduced a Voluntary e-Way Bill Closure facility, allowing stakeholders to close an e-Way Bill after successful delivery of goods.

Who can close the e-Way Bill?

• Supplier

• Recipient

• Transporter

• Driver or authorised person whose mobile number has been registered for this purpose.

Closure may be completed e-Way Bill-wise or date-wise. APIs have also been released for ERP integration.

Practical Considerations

Although it is currently voluntary, the closure process introduces an additional operational step for businesses choosing to adopt it. Organisations may need to establish internal procedures, assign responsibilities and modify ERP workflows. While there is currently no notification indicating that closure will become mandatory, businesses may wish to monitor future regulatory developments.

3. ERP and System Readiness

GSTN has advised ERP vendors, GST Suvidha Providers (GSPs), Application Service Providers (ASPs) and API Integrators to update systems, test revised APIs and complete necessary configuration changes before implementation.

4. Industry Concerns Beyond Compliance

Trade bodies have expressed concerns that mandatory disclosure of the consignee’s GSTIN could expose commercially sensitive customer information and affect traditional intermediary business models.

• Protection of customer confidentiality.

• Preservation of intermediary business models.

• Potential disintermediation of traders and distributors.

• Impact on stockists, commission agents and MSMEs.

• Possible disruption of established supply chain practices.

Two Perspectives on the GSTN Enhancements

|

GSTN’s Objective |

Industry’s Concern |

|

Improve traceability of goods movement. |

Protect customer confidentiality and commercially sensitive information. |

|

Strengthen data integrity. |

Preserve intermediary business models. |

|

Enhance audit trails and digital compliance. |

Avoid potential disintermediation of traders, distributors and stockists. |

|

Improve system-driven analytics and transparency. |

Safeguard MSMEs and traditional supply chain relationships. |

|

Complete digital lifecycle through voluntary closure. |

Additional operational steps may increase administrative workload. |

What Should Businesses Do Before 1st August 2026?

• Review Bill-To / Ship-To transactions.

• Validate GSTIN master records.

• Update ERP systems and APIs.

• Test revised e-Way Bill workflows.

• Train dispatch, logistics and accounts personnel.

• Evaluate internal processes for voluntary e-Way Bill closure.

• Monitor further GSTN notifications and clarifications.

Conclusion

The latest GSTN enhancements represent another step in the evolution of India’s digital GST framework. While the stated objectives are improved traceability and data quality, industry has also highlighted concerns regarding customer confidentiality, intermediary business models and operational impact. Businesses should use the extended timeline up to 1 August 2026 to prepare their systems and processes while monitoring future developments.