For most salaried employees, tax planning begins with a simple assumption:

“Higher salary means higher income tax.”

“Once your salary crosses ₹12 lakh, paying income tax becomes inevitable.”

“The new tax regime has taken away all deductions.”

“There is very little scope for tax planning for salaried employees.”

These assumptions were largely true under the conventional understanding of salary taxation. However, the introduction of the new tax regime has changed the way salaried employees should approach tax planning.

While the new regime has withdrawn most of the traditional deductions, it has simultaneously retained certain salary-linked benefits that can be effectively utilised through proper compensation structuring. As a result, it is now possible, in specific cases, for a salaried employee to substantially reduce taxable income and, in certain well-structured salary packages, even bring the final income tax liability close to nil on a Cost to Company (CTC) of approximately ₹16 lakh.

This is not a loophole. It is structured compensation planning within the framework of the Income-tax Act.

Let us understand how this works.

Why Salary Structuring Has Become More Important Than Ever

For many years, tax planning for salaried employees revolved around investments under Section 80C, contributions to PPF, life insurance premiums, ELSS and housing loan deductions.

The new tax regime under Section 115BAC of the Income-tax Act, 1961, corresponding to Section 202 of the Income-tax Act, 2025, has significantly altered this approach. Although most traditional deductions are no longer available, a number of important salary components continue to enjoy favourable tax treatment. Consequently, the emphasis has shifted from investment-based tax planning to compensation-based tax planning.

The objective is to legally structure the salary in a manner that maximises the tax-efficient components permitted under the Income-tax Act. Where this results in the taxable income falling below the rebate threshold, the employee may significantly reduce or even eliminate the final tax liability.

Understanding the Difference Between CTC and Taxable Income

CTC represents the total cost incurred by the employer, whereas taxable income is determined after considering the applicable provisions of the Income-tax Act, exemptions, deductions and the tax treatment of various salary components. A well-designed salary structure may therefore contain components that either receive concessional tax treatment or reduce the taxable portion of salary. Understanding this distinction forms the foundation of effective tax planning under the new tax regime.

A Practical Illustration

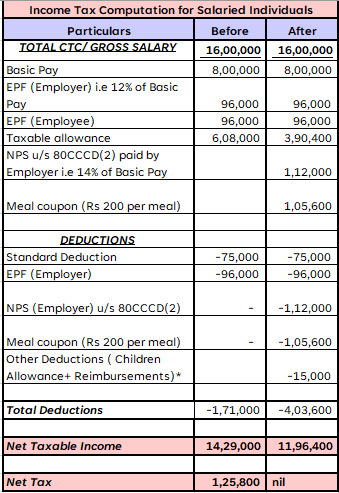

To understand how compensation structuring can influence the final tax liability, consider an illustrative salary structure of a salaried employee having a Cost to Company (CTC) of ₹16 lakh.

The illustration demonstrates how various tax-efficient salary components, when structured appropriately within the framework of the Income Tax Act, may reduce the employee’s taxable income below the threshold prescribed for a rebate under the new tax regime. The actual tax outcome depends upon the employee’s salary structure, employer policies, eligibility and payroll implementation.

Components That Make the Difference

Standard Deduction

The standard deduction of ₹75,000 available under Section 16(ia) of the Income-tax Act, 1961, corresponding to Section 19(1) read with Table Sl. No. 2 of the Income-tax Act, 2025, continues to remain available under the new tax regime.

Employer’s Contribution to EPF

Employer’s contribution towards EPF forms an integral part of many salary structures and, subject to the prescribed limits, receives a different tax treatment from direct salary.

Employer’s Contribution to NPS

Under Section 80CCD(2) of the Income-tax Act, 1961, corresponding to Section 124 of the Income-tax Act, 2025, employer contributions to an employee’s NPS account continue to remain deductible even after opting for Section 115BAC.

Meal Coupons and Meal Cards

Many employers provide meal benefits through recognised providers such as Pluxee, Zaggle SAVE, Edenred, HDFC FoodPlus, ICICI Bank Meal Card, Axis Bank Meal Card, EnKash and Happay FlexiBenefits. These may generally be utilised through authorised restaurants, supermarkets, grocery stores and approved food delivery platforms, subject to employer policy and applicable Income-tax Rules.

Official Reimbursements

Official reimbursements such as internet, mobile and work-from-home communication expenses may continue to receive favourable tax treatment where supported by documentation and linked to official business use.

An Important Caveat

This illustration should not be interpreted as a universal formula. Every employer follows a different compensation policy, and not every salary package contains employer NPS contributions, meal benefits or official reimbursements. Salary restructuring should always be evaluated after considering employer policies, statutory provisions and professional advice.

The Real Takeaway

Professional tax planning is no longer limited to selecting between the old and the new tax regime. Increasingly, it begins at the stage of designing the salary package itself.

Employers and employees who work together to structure compensation within the framework of the Income-tax Act can often unlock significant tax efficiencies while remaining fully compliant with the law.

A well-structured salary is not merely about reducing tax—it is about making compensation more efficient.

View the video on Youtube HERE.